Advertisement

If you have a new account but are having problems posting or verifying your account, please email us on hello@boards.ie for help. Thanks :)

Hello all! Please ensure that you are posting a new thread or question in the appropriate forum. The Feedback forum is overwhelmed with questions that are having to be moved elsewhere. If you need help to verify your account contact hello@boards.ie

Hi there,

There is an issue with role permissions that is being worked on at the moment.

If you are having trouble with access or permissions on regional forums please post here to get access: https://www.boards.ie/discussion/2058365403/you-do-not-have-permission-for-that#latest

There is an issue with role permissions that is being worked on at the moment.

If you are having trouble with access or permissions on regional forums please post here to get access: https://www.boards.ie/discussion/2058365403/you-do-not-have-permission-for-that#latest

What is stopping you from buying a home?

Comments

-

Cool, you do realise you are not just paying 25 quid for the overdraft right?

Of course.

My point is - I'm paying 25 Euro just to have access to the facility (which I want to keep, as it's a useful facility).

My opinion is - why pay for a service you cannot use?

I realise you have a different opinion, but many people have different opinions on different issues. Such is life.") 0

0 -

Dannyboy83 wrote: »Of course.

My point is - I'm paying 25 Euro just to have access to the facility (which I want to keep, as it's a useful facility).

My opinion is - why pay for a service you cannot use?

I realise you have a different opinion, but many people have different opinions on different issues. Such is life.

But if you have the overdraft removed, you dont pay that fee. You are paying money for a service you don't need, its baffling, I'm genuinely attempting to understand your reasoning for this.

The only outcome of this situation is that you are losing money year on year for absolutely no benefit.

In addition if I was evaluating you for a loan, this would be a massive red mark against you. It at the very least implies, you dont understand financial products. Or your behaviours and actions suggest you dont, even if you do.0 -

But if you have the overdraft removed, you dont pay that fee. You are paying money for a service you don't need, its baffling, I'm genuinely attempting to understand your reasoning for this.

The only outcome of this situation is that you are losing money year on year for absolutely no benefit.

But - by your logic, why would anyone ever use any type of credit facility?

In fact, why would I be applying for a mortgage at all by this reasoning.

There is an opportunity cost with everything...0 -

Dannyboy83 wrote: »But - by your logic, why would anyone ever use any type of credit facility?

In fact, why would I be applying for a mortgage at all by this reasoning.

There is an opportunity cost with everything...

Eh, you apply for credit when you don't have the reserves yourself to buy something..... you have the money. So you are taking the penalties of borrowing when its not required.0 -

Dannyboy83 wrote: »There have been a number of articles recently saying houses have become affordable again etc.

e.g.

http://www.irishexaminer.com/breakingnews/ireland/international-house-prices-study-irish-homes-affordable-again-537065.html

Just wondering, for the people who still intend to buy a home in Ireland at some stage,

A) do you feel that houses have become affordable again and") what is stopping you from buying?

what is stopping you from buying?

Yes definitely.

I know you are talking about houses. But take apartments. I could buy an apartment outright at the moment.

Why i hesitate is that i feel prices are still likely to fall. I do not want to lose value.

Since buying a home is no longer an investment i feel i look at it differently now. Is it worth it?

I never want a mortgage. I like being debt free. There is a huge advantage to it at the moment. My career is the priority.

I may not stay in Ireland and that also would be a factor.

I might consider buying abroad at some point as my work is location independent.0 -

Dannyboy83 wrote: »Thank you, but you don't need to point that out.

As I've already explained several times - I met with the bank's advisors several times to ensure I was satisfying all their criteria.

It seems like I do need to point this out, because you cannot see the risk inherent in your approach to meeting their criteria.Dannyboy83 wrote: »At my next bank, I will not avail of the overdraft facility (explain how this makes the new bank profitable again?

Banks don't make profits off account charges & fees. They make them off loans & interest, which they fund using deposits.Dannyboy83 wrote: »The mortgage advisors clearly outlined the criteria - I wrote them above for you.

12k minimum per year was the requirement. This is standard

Are you familiar with the current mortgage approval process?

I write FSI software for a multinational, lending and account origination give us massive headaches because of the differences between regulations. I'm vaguely aware of the kind of criteria that banks don't tell their customers about.Dannyboy83 wrote: »I think I see where you're getting confused now.

I agree with that statement - but how does that apply to me?

Do the math here.

Net worth increased by 14k.

Your net worth may have increased by 14k but that will have been because of diverting funds from other costs to savings, not the use of your overdraft.

I could do the same if I redirected all outgoings on my rent & bills and cut out entertainment (e.g. my golf membership - €750) to savings. But since I don't live at home, the cutting rent & bills isn't an option that isn't an option.Dannyboy83 wrote: »An overdraft is for spending more than you have in your current account - not more than you *have*.

How could my net worth have increased if I spent more than I had?

If you have it, then why do you need to use a facility that is costing you €25 p.a. + 15c on the euro?

Seriously an overdraft is supposed to be an insurance policy, you are using it as a line of credit.Dannyboy83 wrote: »I could just as easily not use an overdraft, instead use a credit card and pay that off in full every month instead.

Wrt your mortgage appliciton, you'd have been better off.Dannyboy83 wrote: »p.s.

You also contradict your previous point - how can the money management be poor if the savings are excessive? Unless cash flow management is explicitly considered poor money management (in which case - why do AIB provide the Masterplan product?)

Last attempt - you're spending more than is in your account in order to increase what is in another account.Dannyboy83 wrote: »AIB never suggested that use of their overdraft facility was a problem during any of the meetings I had.

Why would they, unless it has to be explained to you that an overdraft is a loan - and banks look lending and spending historiesDannyboy83 wrote: »Oh, come on.

Is that the green eyed monster I see here?:rolleyes:

Hell no, I wouldn't like to try to divert an additional 12k of my income.Dannyboy83 wrote: »With regard to "Flag#3", my savings come from my sole income.

There is an audit trail from my AIB current account to my AIB deposit account, showing my savings transferred on the 1st day of every month.

It was purposely structured in this manner in November 2011, at the behest of AIB advisors, to eliminate any possibility of what you are suggesting above.

Should have put that in your initial post. Large sudden influxes of money is one of the flags raised for mortgages, so without the knowledge that the bank structure the savings for you it looks like something that would trip up an application.Dannyboy83 wrote: »With regard to Flag#1, my father has been overdrawn since the 70s and has acquired several properties outright during this time.:pac:

The fact is that AIB have become utterly risk averse.

Oh plueezze, AIB were worse than Anglo when it came to giving out loans. They never had anywhere near decent risk analysis. If they did we wouldn't be bailing them out again - this is the second bailout they have gotten in the past 30 years!

The fact is now that you are falling foul of rules that should have been implemented years ago and blaming AIB for it.0 -

antoobrien wrote: »If you have it, then why do you need to use a facility that is costing you €25 p.a. + 15c on the euro?

THIS! It makes no ****ing sense.0 -

Net point: You remove the charge, you make the bank less profitable."Banks don't make profits off account charges & fees"Your net worth may have increased by 14k but that will have been because of diverting funds from other costs to savings, not the use of your overdraft.

That's why they called Rent, "dead money" for so long, remember?

Of course, it's not. It's an opportunity cost.

I don't have the privacy you have, I sacrificed it.I could do the same if I redirected all outgoings on my rent & bills and cut out entertainment (e.g. my golf membership - €750) to savings. But since I don't live at home, the cutting rent & bills isn't an option that isn't an option.

So share with another couple.

Live somewhere cheaper.

Stop drinking, smoking, playing golf.

Entertainment - what is that? I don't remember.

You don't save 50% of your net income without sacrifice.Hell no, I wouldn't like to try to divert an additional 12k of my income.

"Diverting my income? You'd swear I robbed it! LOL!

Would that get me a red mark too, would it? :pac:

I do believe I had to save it sir!

This thread has become awkward. Farewell.

/thread

p.s.

Anyone applying to AIB, please be advised that they are utterly risk averse.0 -

Dannyboy83 wrote: »Net point: You remove the charge, you make the bank less profitable.

Charges are almost irrelevant to banks profitability, which is why they cut them out during the boom. They badly need the money now to offset losses on loans and cost of the bailout, which is why they've been re-instated.Dannyboy83 wrote: »That's why they called Rent, "dead money" for so long, remember?

Rent was never dead money, it kept a roof over the head. You just had less control over it than a mortgage. On the other hand there are now a lot of people wishing they didn't have the mortgage and would prefer to rent.Dannyboy83 wrote: »So share with another couple.

Live somewhere cheaper.

Stop drinking, smoking, playing golf.

Entertainment - what is that? I don't remember.

You don't save 50% of your net income without sacrifice.

Don't smoke, don't spend much on drink already share. But then this is about your spending habits not mine.

If push came to shove though I'd keep the golf and stop drinking.Dannyboy83 wrote: »"Diverting my income? You'd swear I robbed it! LOL!

Would that get me a red mark too, would it? :pac:

Oh stop being childish, that attitude will have counted against you with the bank as well, becuase they have enough people with "entitlement syndrome" on their books.

You had money that you were spending on something else, you chose to spend it on something different. Use of the word divert saved a few words.Dannyboy83 wrote: »I do believe I had to save it sir!

Not criticizing your choice of savings, criticizing your attitude towards people that are trying to help you see how your application may have failed.Dannyboy83 wrote: »Anyone applying to AIB, please be advised that they are utterly risk averse.

Given the few details you've put up here, if I were a loan/credit officer (in any bank) I wouldn't approve a mortgage to you. There are too many red flags to overlook.0 -

antoobrien wrote: »Use of the word divert saved a few words.

Far enough, it just came across rather differently when I was reading it.

I take all points onboard anyway, Thank to all contributors.

I don't have it in me to continue on the thread, know what I need to do and would rather just get on with it.

Thanks all 0 -

Advertisement

-

Anyways back on topic...

Whats stopping me buying a house:- The quality to houses built during the boom is atrocious (items signed off on that was not carried out to spec (e.g septic tanks) badly hung doors, bare skim of plaster, poor wiring ( metal sockets not earthed), poor plumbing list goes on.

- I believe the property market is only at the midst of the decline. I expect it to continue until at least 2015 and remain at the bottom for about 5 years until some stability emerges.

- Any property that that I would purchase would be a liability due to property tax, water rates and maintenance.

- I am currently working abroad (in the UK earning better money than at home with more disposable income). There are little suitable opportunities in Ireland in engineering better from a financial aspect to stay overseas for the medium.

I place more emphasis on flexibility at the moment rather than bricks and mortar. I could possibly return in 10 years provided this whole mess is sorted out and suitable job opportunities becoming available.0 -

I still have no confidence in the market or the Irish or Eurozone economic systems. Way too much uncertainty and I could need to emigrate if it all gets worse so, there's no way I'm tying myself down!

I couldn't possibly justify buying while having those kinds of vibes!0 -

I'm no financial expert (but then again, given the last few years in this country/the EU/the global market, IS there even such a thing?) but I'd have to side with Dannyboy above

- He's had regular meetings with AIB's advisers and setup his accounts accordingly

- He's saved 15k in a year.. no small achievement in itself

.. yet they're whinging about his use of a service that he in fact pays them MORE money for and which is always cleared down to zero at the start of each month (assuming his wages are paid into the same a/c).

I don't see the problem here except that they simply don't want to give him the money and are pulling out any excuse they can to justify it, yet still claim that they're "open for business" :rolleyes:

But at least he's doing the right thing and rather than just bitching impotently about it on the Internet, he's taking his business elsewhere.

Hope it works out for you

Anyway, to answer the original question...What is stopping you from buying a home?

Few things really...

1. Although a Dub born and bred, I must've been passed over for the "must own a house/apartment, must get on property ladder, renting is dead money" gene that got the country into this mess (alongside the thought that you too can become a property magnate of course)

This means that, while sure I wouldn't MIND having my own property, it has to fulfil a number of criteria first.

(a) It has to be somewhere where I want to live, not just can afford to. I spent most of 2011 doing a 1000 km weekly commute to work and while it was motorway 95% of the way and only took about an hour door-to-door, the running costs of doing that are ridiculous - plus it IS nice being home (now) before 5pm

(b) Related to the above, it has to be near work yes but also my friends, family, decent shops, facilities etc. I've no interest in living in the back-end of

nowhere with 500 others in a half-finished housing estate with the nearest shop being maybe 10/20 mins drive away.

(c) I have to be able to afford it. By this I mean being able to make the repayments without simply ending up with no life and working only to pay off the mortgage. Not for me thanks. Plus I don't think the prices have hit bottom anyway what with the situation created by NAMA stockpiling property, the artificial floor in the rental market as a result of RA etc

If I could find a house (and a lender actually willing to lend!) then sure, I might take the plunge but there's a few other points against me at this stage...

- I was unemployed for most of 2010 and so like anyone else in that situation, I struggled a lot to make ends meet. As I've said on this forum before, what's often forgotten here is that your bills and debts don't just disappear with your salary.. nor can you just say "Ah shure I'll pay ye back when I get a new job boss" - life becomes a stressful dance of trying to pay everyone just enough each month to keep them off your back another while.

As a result, savings are non-existent.

- I have a loan that I took out in the "good times" and was comfortably able to pay in those days, but with the above change in circumstances it had to be restructured and is still being paid off. I also had a big credit card bill too that has now been rolled into that loan agreement, but it'd no doubt go against me - despite my having been open and honest with them about the situation from day 1, and being proactive in offering to pay more when my circumstances improved.

- I'm on the "bad" side of 35 so even qualifying for a mortgage would take what.. another 5/10 years to build up this ideal banking history they are beating poor Dannyboy over the head with above :rolleyes:. I'll be too old at that point to qualify I'm sure... ah well, I guess maybe I should have accepted the "pre-approved 300k mortgage" they kept offering me every few weeks in 2006

But in the end, I suppose my primary reason is that I just don't have this Irish NEED to own my own place. I do think that the rental market needs serious reform though and a shift away from the Irish model of short-term tenancies of a year or two (on average) to one where 5/10/20 year arrangements are the norm like even up North and in Europe so that you CAN make your accommodation a home as opposed to the laughable setup where the house-proud landlord whinges about putting a feckin nail in a wall to hang a picture :rolleyes: and hums and haws about changing the color scheme etc - yet still expects the tenant to cough up the inflated rent on time anyway.

We have a lot of things we need to do in this country, but still obsessing about property isn't it.0 -

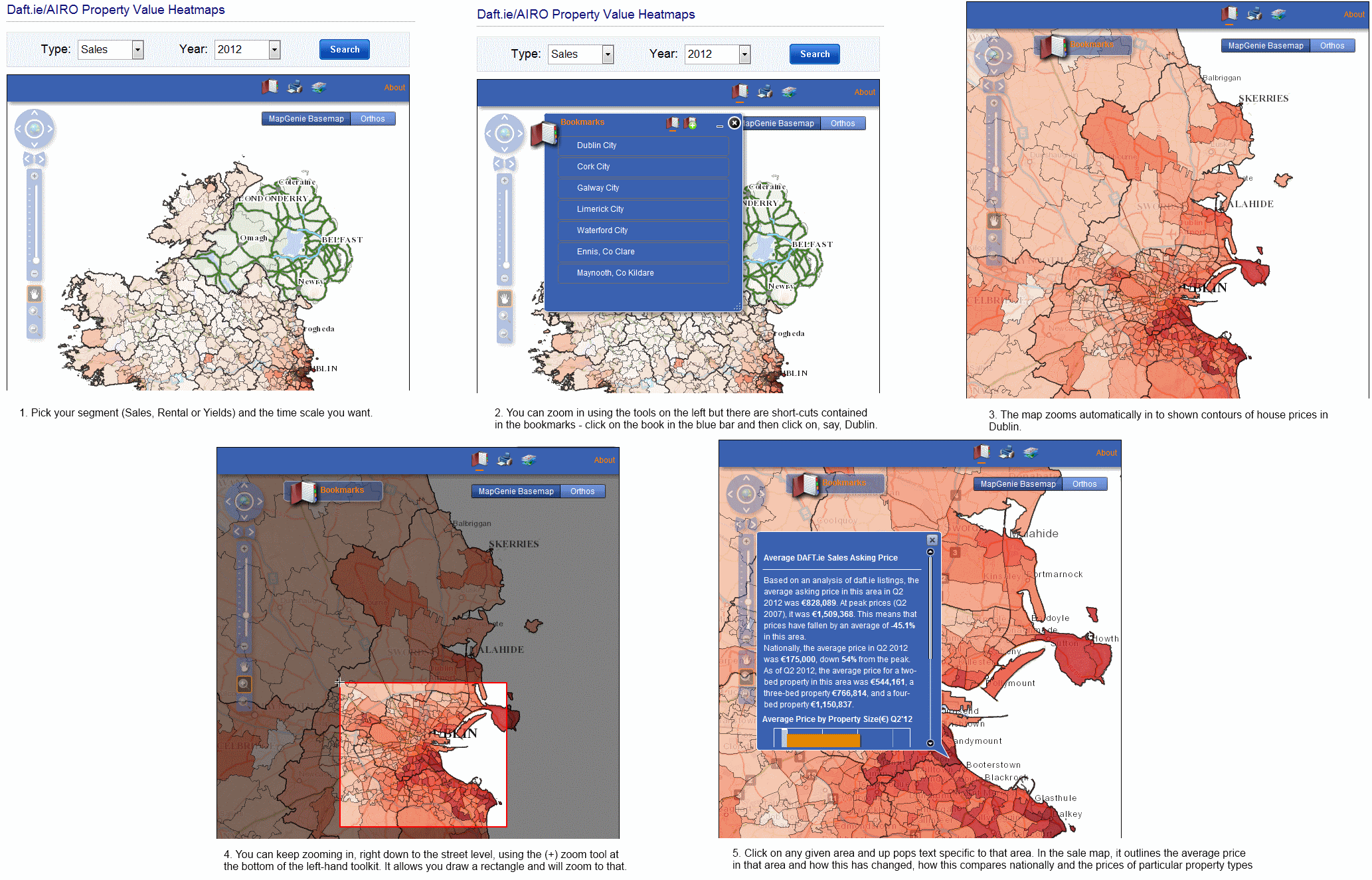

Saw this the other day, I'm not sure where from originally; heat map of property prices in Ireland:

http://www.ronanlyons.com/wp-content/uploads/2012/07/Basic-Map-Guide.png

http://www.ronanlyons.com/2012/07/02/get-them-while-theyre-hot-or-cold-heatmaps-of-property-values-in-ireland-now-available/

http://www.daft.ie/research/?request=research0 -

Pros and cons to both.

Pros to buy- Property Taxes/water charges etc will be passed onto the renter whether they like it or not with some landlords making it a larger increase in your rent then necessary to bump there rent up.

- Prices have started to stabilize in my opinion

- Rents will increase most years while your mortgage repayments shouldn't vary too much and over the years the amount you are paying back becomes a smaller amount of your income.

- Option to throw more money against the mortgage in the good times to help when you get to the bad times. Example paying back more than your monthly repayment while keeping the duration the same lowering your monthly repayment.

- Renting allows a flexibility to move when you need to and downsize your expenses in a hurry(New Job in a different location or lost your Job completely).

- Landlord is there to fix things like broken dishwashers etc.

- I have no idea where I'm going to be in the world in the next 3-5 years have no family so no need to.

- It can be difficult at the moment to sell on a house/apartment in a timely manner if you need to upgrade(kids or something)

- Large deposit needed between 8-15% I think?

At the moment I have no deposit and not looking like I'm going to be able to afford to contribute to one anytime soon and I don't know if my future is in Dublin, Galway, Cork, Canada etc.

These are my biggest issues at the moment.0 -

everdead.ie wrote: »Pros and cons to both.

- Property Taxes/water charges etc will be passed onto the renter whether they like it or not with some landlords making it a larger increase in your rent then necessary to bump there rent up.

- Prices have started to stabilize in my opinion

- Rents will increase most years while your mortgage repayments shouldn't vary too much and over the years the amount you are paying back becomes a smaller amount of your income.

- Option to throw more money against the mortgage in the good times to help when you get to the bad times. Example paying back more than your monthly repayment while keeping the duration the same lowering your monthly repayment.

1. Water charges paid by tennant/Property tax some landlords may try to pass it on with limited success.

2. In very limited areas

3. This is a biggy, Rents will not rise substantially. We are still pretty much in a deflationary environment, Any inflationary pressure is coming from the State Services.

Mortgage repayments will increase substantially overtime The current base rate is 0.75% which is an emergency rate. Normal Rates would be between 4.5 to 6% add in the Banks Markup and you have normal rates at 8.5% to 10%.

Bear in mind that the banks have huge losses not yet realised on there books and this could add another 2 to 3% on to their mortgage rates.

The base rate is decided by Frankfurt, Now imagine a situation where there is rampant inflation in Germany and Ireland remains in a deflationary/Stagnant environment. (This is a scenario that is highly likely) Frankfurt increases the base rate substantially to cool their inflation. Irish borrowers are crucified.

Anyone who follows your advise on pro's to buying is guaranteed to get wiped out in my opinion0 -

everdead.ie wrote: »Pros and cons to both.

Pros to buy- Property Taxes/water charges etc will be passed onto the renter whether they like it or not with some landlords making it a larger increase in your rent then necessary to bump there rent up.

- Prices have started to stabilize in my opinion

- Rents will increase most years while your mortgage repayments shouldn't vary too much and over the years the amount you are paying back becomes a smaller amount of your income.

- Option to throw more money against the mortgage in the good times to help when you get to the bad times. Example paying back more than your monthly repayment while keeping the duration the same lowering your monthly repayment.

- Renting allows a flexibility to move when you need to and downsize your expenses in a hurry(New Job in a different location or lost your Job completely).

- Landlord is there to fix things like broken dishwashers etc.

- I have no idea where I'm going to be in the world in the next 3-5 years have no family so no need to.

- It can be difficult at the moment to sell on a house/apartment in a timely manner if you need to upgrade(kids or something)

- Large deposit needed between 8-15% I think?

At the moment I have no deposit and not looking like I'm going to be able to afford to contribute to one anytime soon and I don't know if my future is in Dublin, Galway, Cork, Canada etc.

These are my biggest issues at the moment.1. Water charges paid by tennant/Property tax some landlords may try to pass it on with limited success.

2. In very limited areas

3. This is a biggy, Rents will not rise substantially. We are still pretty much in a deflationary environment, Any inflationary pressure is coming from the State Services.

Mortgage repayments will increase substantially overtime The current base rate is 0.75% which is an emergency rate. Normal Rates would be between 4.5 to 6% add in the Banks Markup and you have normal rates at 8.5% to 10%.

Bear in mind that the banks have huge losses not yet realised on there books and this could add another 2 to 3% on to their mortgage rates.

The base rate is decided by Frankfurt, Now imagine a situation where there is rampant inflation in Germany and Ireland remains in a deflationary/Stagnant environment. (This is a scenario that is highly likely) Frankfurt increases the base rate substantially to cool their inflation. Irish borrowers are crucified.

Anyone who follows your advise on pro's to buying is guaranteed to get wiped out in my opinion

At the end of the day it is all a matter of opinion. For anybody the question is that are at or near the bottom of the housing bust just like we had boomers (those that never say house prices falling) we will also have busters (those who can never see prices rising again)

It may well be that the next 12 months will be the time to buy. Why????

It is often better to buy on the way down rather than on the way up you have more choice. It looks like that house that will be thrown on the market by the insolvency laws/NAMA may be snapped up by big property firms from abroad who will buy in muliples.

My own opinion was that in the case of an overcorrection that vulture funds from abroad and professional landlords would snap up value and rent them out.

Rental prices have remained remarkably stable throughout the bust so investors will have confidance with present yields while they may not rise substancially it also looks like they will not fall.

Intrest rates in the shortterm looks like they may again fall rather than rise it also looks like there will be no substancial rise in the medium term. It is hard to see them being above 2% in 3 years time. Inflation is the friend of the property owner. Inflation means that wages will rise and your property's value as well unless there is some massice change in economic fundmentals. Also base rates have little comparrison to mortgage rates at present most new loans are 3.5% above the base so comparing base rates is not realistic. Yes rates could hit 10% however they could also remain at 4-4.5% for the next 10 years (both senario's are unlikly). As intrest rates rise banks as they become more solvent may well reduce their margin on mortgage's.

If you wish to buy a house now may be as good if not a better time than any in the last 10 years. It look like houses are below the cost of construction.

My one piece of advice is that if you do make sure you get a good structural survey done (not neccessiarly by an engineer a good tradesman may see defects faster, you only need the engineer for the loan)0 -

I'm not buying where I am because it's at the tail end of a property bubble now.

I'm not buying in Ireland because I don't live there like many emigrants :cool:.

I might buy in Ireland if I had more cash but only some of us emigrants are able to do that.0 -

1. Water charges paid by tennant/Property tax some landlords may try to pass it on with limited success.

2. In very limited areas

3. This is a biggy, Rents will not rise substantially. We are still pretty much in a deflationary environment, Any inflationary pressure is coming from the State Services.

Mortgage repayments will increase substantially overtime The current base rate is 0.75% which is an emergency rate. Normal Rates would be between 4.5 to 6% add in the Banks Markup and you have normal rates at 8.5% to 10%.

Bear in mind that the banks have huge losses not yet realised on there books and this could add another 2 to 3% on to their mortgage rates.

The base rate is decided by Frankfurt, Now imagine a situation where there is rampant inflation in Germany and Ireland remains in a deflationary/Stagnant environment. (This is a scenario that is highly likely) Frankfurt increases the base rate substantially to cool their inflation. Irish borrowers are crucified.

Anyone who follows your advise on pro's to buying is guaranteed to get wiped out in my opinion

On number 1 the landlords can't afford not to pass it on.

Depending on where you are living renting can be more expensive than buying if I bought the current property I'm renting for 10% more than two(bigger) neighbouring apartments were sold for in 2010 I'd see my rent/repayment drop by 15%(based on AIB's owner occupier calculator).

I should also clarify I live in the city and the misses doesn't want to live in the suburbs and I don't want to buy in the city(for fear that if we decide to have a family we could be stuck with a property we can't sell or get significantly less than we paid for it that won't fit a family.)0 -

Advertisement

-

Kaiser2000 wrote: »

Few things really...

1. Although a Dub born and bred, I must've been passed over for the "must own a house/apartment, must get on property ladder, renting is dead money" gene that got the country into this mess (alongside the thought that you too can become a property magnate of course)

This means that, while sure I wouldn't MIND having my own property, it has to fulfil a number of criteria first.

(a) It has to be somewhere where I want to live, not just can afford to. I spent most of 2011 doing a 1000 km weekly commute to work and while it was motorway 95% of the way and only took about an hour door-to-door, the running costs of doing that are ridiculous - plus it IS nice being home (now) before 5pm

(b) Related to the above, it has to be near work yes but also my friends, family, decent shops, facilities etc. I've no interest in living in the back-end of

nowhere with 500 others in a half-finished housing estate with the nearest shop being maybe 10/20 mins drive away.

(c) I have to be able to afford it. By this I mean being able to make the repayments without simply ending up with no life and working only to pay off the mortgage. Not for me thanks. Plus I don't think the prices have hit bottom anyway what with the situation created by NAMA stockpiling property, the artificial floor in the rental market as a result of RA etc

If I could find a house (and a lender actually willing to lend!) then sure, I might take the plunge but there's a few other points against me at this stage...

- I was unemployed for most of 2010 and so like anyone else in that situation, I struggled a lot to make ends meet. As I've said on this forum before, what's often forgotten here is that your bills and debts don't just disappear with your salary.. nor can you just say "Ah shure I'll pay ye back when I get a new job boss" - life becomes a stressful dance of trying to pay everyone just enough each month to keep them off your back another while.

As a result, savings are non-existent.

- I have a loan that I took out in the "good times" and was comfortably able to pay in those days, but with the above change in circumstances it had to be restructured and is still being paid off. I also had a big credit card bill too that has now been rolled into that loan agreement, but it'd no doubt go against me - despite my having been open and honest with them about the situation from day 1, and being proactive in offering to pay more when my circumstances improved.

- I'm on the "bad" side of 35 so even qualifying for a mortgage would take what.. another 5/10 years to build up this ideal banking history they are beating poor Dannyboy over the head with above :rolleyes:. I'll be too old at that point to qualify I'm sure... ah well, I guess maybe I should have accepted the "pre-approved 300k mortgage" they kept offering me every few weeks in 2006

But in the end, I suppose my primary reason is that I just don't have this Irish NEED to own my own place. I do think that the rental market needs serious reform though and a shift away from the Irish model of short-term tenancies of a year or two (on average) to one where 5/10/20 year arrangements are the norm like even up North and in Europe so that you CAN make your accommodation a home as opposed to the laughable setup where the house-proud landlord whinges about putting a feckin nail in a wall to hang a picture :rolleyes: and hums and haws about changing the color scheme etc - yet still expects the tenant to cough up the inflated rent on time anyway.

We have a lot of things we need to do in this country, but still obsessing about property isn't it.

Well said,that Kaiser2000....:)

A tour-de-force of significant proportions,most of which will be taken as threatening by those who are lying in the long-grass biding their time before buying "at the right time".

But,as the Kaiser sez,for as long as Irelands future is woven into the likes of NAMA,s fabric then it's a hopeless case....:(Men, it has been well said, think in herds; it will be seen that they go mad in herds, while they only recover their senses slowly, and one by one.

Charles Mackay (1812-1889)

0 -

I'd rather rent or build a house than buy one. Renting would all I could afford but even I couldn't afford to move out without some decent income.0

{kind=link}

Advertisement