Advertisement

If you have a new account but are having problems posting or verifying your account, please email us on hello@boards.ie for help. Thanks :)

Hello all! Please ensure that you are posting a new thread or question in the appropriate forum. The Feedback forum is overwhelmed with questions that are having to be moved elsewhere. If you need help to verify your account contact hello@boards.ie

Hi all! We have been experiencing an issue on site where threads have been missing the latest postings. The platform host Vanilla are working on this issue. A workaround that has been used by some is to navigate back from 1 to 10+ pages to re-sync the thread and this will then show the latest posts. Thanks, Mike.

Hi there,

There is an issue with role permissions that is being worked on at the moment.

If you are having trouble with access or permissions on regional forums please post here to get access: https://www.boards.ie/discussion/2058365403/you-do-not-have-permission-for-that#latest

There is an issue with role permissions that is being worked on at the moment.

If you are having trouble with access or permissions on regional forums please post here to get access: https://www.boards.ie/discussion/2058365403/you-do-not-have-permission-for-that#latest

Writing off mortgage debt

Comments

-

StudentDad wrote: »I have to sayI find myself with very little sympathy for those who are in arrears with mortgages and face repossession.

Individuals and couples chose to purchase a property. They chose to obtain a mortgage. They were made aware of the consequences of non-payment of the mortgage. They should have known that the property market was a self-inflating bubble with little or no value supporting it. That being the case the idea of some sort of debt forgiveness scheme abhors me. Who pays for this? The European taxpayer?

People chose to take out loans of whatever amount over x number of years. Adults supposedly capable of making rational decisions. I don't care if the bank was 'giving' the money away at 'reasonable' or 'insanely low levels of interest.' Last time I checked individuals still have the option to say 'no' - Accepting an offer of a bank loan is not mandatory.

SD

Thats a pretty harsh view thats encapslates the really agressive edge of pure capatilism in that every man women and child is for themselves and the strongest survive and the weak perish.

People took out loans and bought houses because employment was good and prospects and confidence was high. There was optomism about the future. The overall risk perceived was low.

I worked in construction and my spoken fears about the end of the bubble were laughed at and derided by senior managers and experts from a variety of fields including directors, consultants and developers.

The banks were lending and the government was bullish (even suggesting that anyone not on the gravy train should suicide themselves!) and most experts were agreed that everything would be ok.

If it was that obvious what was going to happen to an economy then let me know what the sure fire 100% events that will happen in the future are and then you can personally guaratee them if it's all so easy to predict!

We have all been brought up to pay ourway but what irks me most is the total lack of humanity a lot of people on this thread have towards their fellow man. People are financially crippled and socially trapped unable to move. Growing families are sufferring in less than ideal propertys they should of moved out of.

If people here were to spend some time researching what money is and where it all comes from they might be a little more pragmatic and not just accept the monetary paradigm without question which is basically where we are all today.

Money is really nothing more than an arbitary number we assign to value everything in our lives. The monetary system is designed in such a way that defaults and poverty are built in to happen yet we accept it even though it causes suffering to people.

We are all in the belief that our governments have bailed out the banks and saved them. The reality as far as I can see is that europe has become enslaved to them as its population must work and toil well into old age to achieve only the most basic quality of life.0 -

So because some people misjudged the risk, they should be let off their commitments, and everybody else should be penalised? :confusedThats a pretty harsh view thats encapslates the really agressive edge of pure capatilism in that every man women and child is for themselves and the strongest survive and the weak perish.

People took out loans and bought houses because employment was good and prospects and confidence was high. There was optomism about the future. The overall risk perceived was low.

Clearly it's self evident that we haven't all been brought up to pay our way - lots of people habitually expect everyone else to pay for them instead. What irks me however is this pretence that those who expect people to pay for what they have taken or else surrender it is that we are somehow inhuman. Nonsense. There is a real social cost for every person who is let get away without paying their debts. Every euro that is spent subsidising people to stay in their bubble houses or writing off their bubble debts is a euro that can't be spent on special needs teachers or paediatric nurses or Gardaí or whatever else. In addition, it teaches everybody that the next time there's some sort of bubble mania going on, they had better take part because it's a one-way bet - if they make money they keep it, and if they lose all their money then their neighbours will be taxed to the back teeth to get them their money back. This will just make the next bubble frenzy even more damaging, which is quite a frightening thought when you consider that the current one has wiped out all our banks, huge chunks of our pensions, doubled our national debt and cost us a large part of our sovereignty.We have all been brought up to pay ourway but what irks me most is the total lack of humanity a lot of people on this thread have towards their fellow man. People are financially crippled and socially trapped unable to move. Growing families are sufferring in less than ideal propertys they should of moved out of.

I'm sure it makes some people feel warm and fuzzy inside thinking that letting people away with their mistakes and/or greed makes them a better person, but this is a foolish attitude in the long-term - like a parent who thinks that never criticising or punishing their children will mean they turn into model citizens. The reality is that stupid decisions need to have bad results and good decisions need to have positive results - the alternative is to incentivise stupidity and punish intelligence. What kind of society does that create?0 -

Thats a pretty harsh view thats encapslates the really agressive edge of pure capatilism in that every man women and child is for themselves and the strongest survive and the weak perish.

People took out loans and bought houses because employment was good and prospects and confidence was high. There was optomism about the future. The overall risk perceived was low.

I worked in construction and my spoken fears about the end of the bubble were laughed at and derided by senior managers and experts from a variety of fields including directors, consultants and developers.

The banks were lending and the government was bullish (even suggesting that anyone not on the gravy train should suicide themselves!) and most experts were agreed that everything would be ok.

If it was that obvious what was going to happen to an economy then let me know what the sure fire 100% events that will happen in the future are and then you can personally guaratee them if it's all so easy to predict!

We have all been brought up to pay ourway but what irks me most is the total lack of humanity a lot of people on this thread have towards their fellow man. People are financially crippled and socially trapped unable to move. Growing families are sufferring in less than ideal propertys they should of moved out of.

If people here were to spend some time researching what money is and where it all comes from they might be a little more pragmatic and not just accept the monetary paradigm without question which is basically where we are all today.

Money is really nothing more than an arbitary number we assign to value everything in our lives. The monetary system is designed in such a way that defaults and poverty are built in to happen yet we accept it even though it causes suffering to people.

We are all in the belief that our governments have bailed out the banks and saved them. The reality as far as I can see is that europe has become enslaved to them as its population must work and toil well into old age to achieve only the most basic quality of life.

It's nothing to do with "aggressive capitalism". It's called paying back what you owe and not expecting something you can't/won't pay for. Basic social justice in other words. I consider myself centre-left politically and don't mind paying out welfare to those who need it most. As any card-carrying left-winger will tell you, capitalism is basically one gigantic scam to serve the interests of a handful of rich elites like Sean Fitzpatrick. But for it to operate as a scam, it needs enough gullible people to buy into it, and too many did during the boom times. I'm not talking about you personally. I'm just saying...

I also consider it basic inhumanity for someone to expect their neighbours to pay their mortgage for them while many of those people do not even own a house themselves. It's basically another form of undeserving welfare that the country cannot afford.

As another poster just said, if someone cannot afford to pay their mortgage at the end of the month, let them trade down to renting for less.0 -

Some posters see foreclosure / loss of peoples’ homes as the only viable option and seem to have a closed mind to any other solutions to the mortgage arrears issue.

Certainly, in extreme circumstances, where there is no hope of loans ever being repaid, foreclosure and loss of home may be the only answer.

But there are other options, for example the “split mortgage“ concept, which takes a long term view of the value of the property and increasing income (and recalculated repayments) over the mortgagee’s working life, resulting in positive equity at the end of 25 or 30 years (worked examples are included in the Mortgage Arrears report http://www.finance.gov.ie/documents/publications/reports/2011/mortgagearr2.pdf).

The report outlines other solutions – worth consideration – and recent press reports indicate that these being worked on between the lending banks and the Central Bank.

Key recommendations of the report include the following:

Guiding principles:

• Those who can discharge their mortgage obligations must do so

• There is no entitlement to a particular solution and solutions have consequences

• There are unsustainable situations and unfortunately it is inevitable that people will lose their homes; this needs to be minimised

Develop a range of practical solutions:

• A blanket debt forgiveness scheme is not recommended

• A range of solutions are recommended. These and others need to be further developed, over time, by the banks.

• Case by case approach required

• Decision tree approach to facilitate assessment

A variety of solutions, such as those outlined in the report, all with consequences for the mortgagee, appears to me as the best of a bad choice set. Much as I believe that people should pay for their mistakes, I do not believe that immediate mass mortgage foreclosures is either a just or politically acceptable solution.0 -

Monty Burnz wrote: »Ok, seeing as neither of us can manage more than anecdotes, we'd better let this one slide!

")

Agreed!The negative equity is irrelevant in that you can just as easily say that the person with equity in their home can move and have a load of cash in their pocket. So what? It's not like not repossessing people makes their negative equity go away, is it?

Its hardly irrelevant when somone with negative equity hanging over their head following a repossession will both have to rent somewhere to live and repay the negative equity to the bank. Unless, of course, you support the automatic write down of negative equity in these circumstances. If so then you are correct there is no difference between a renter and an owner so let the purge begin!Renters can f*ck off, while owners (of stuff they aren't paying for) are treated like blameless victims of famine and callous colonial indifference - which is of course nonsense.

Yes of course its nonsence if owners are allowed to continue to live in their mortgaged homes mortgage free but not too many are advocating this extreme end of the spectrum approach. What is being advocated by many is a proactive approach whereby mortgage owners in trouble are offered options such as interest only for a period, a lengthening of the mortgage period, a write down of the mortgate payment but with the balance being repaid on sale of house/death of mortgate holder, etc, etc, None of these option involve a freebie for the mortgage holder but they would allow some more disposable income for the mortgate holder which could be spent in the economy while at the same time alleviate the pressure on the inevitable mortgage default if things are left as they are. Which is better a dead mortgate of a live restructured one where banks are getting paid?0 -

Advertisement

-

MysticalRain wrote: »It's nothing to do with "aggressive capitalism". It's called paying back what you owe and not expecting something you can't/won't pay for. Basic social justice in other words. I consider myself centre-left politically and don't mind paying out welfare to those who need it most. As any card-carrying left-winger will tell you, capitalism is basically one gigantic scam to serve the interests of a handful of rich elites like Sean Fitzpatrick. But for it to operate as a scam, it needs enough gullible people to buy into it, and too many did during the boom times. I'm not talking about you personally. I'm just saying...

I also consider it basic inhumanity for someone to expect their neighbours to pay their mortgage for them while many of those people do not even own a house themselves. It's basically another form of undeserving welfare that the country cannot afford.

As another poster just said, if someone cannot afford to pay their mortgage at the end of the month, let them trade down to renting for less.

At no point have I advocated that the state or tax payer should bear the burden of these loans. In fact I was totally against the state bailing out a private profit making company through the banking guarantee scheme.

There are many different individual circumstances of people in different circumstances. For example: -

1/ people and families who are in ghost estates. never any hope of selling or moving or renting. Anyone who thinks they should shut up and pay for the rest of their lives in such awful conditions is just awful IMHO.

2/ Young couples and families who bought small just to get on the ladder and now are stuck in massive -ve equity with a growing family.

3/ people who stuck there knecks out too far because they literally believed that property was as easy as printing your own money.

and many others inbetween.

At least if we had a situation where people could in certain circumstances hand back the keys then they would have a chance of making a +ve difference to the economy and society.

I dont believe for a second that everyone would just up and try to do that as people homes mean more to them than just a place to stay.

Let the banks, many of whom have been in existence before I was I born and will be long after I die take this property and take a long term view as to recovering their 2 cents from it.

Let the people who have a short and limited time on this planet get on with their lives and have a chance at happiness.0 -

Unfortunately you don't seem to recognise that the cost of bailing out the foolish and the unfortunate will be borne by everybody - if it wasn't going to cost us billions, I'd be all for it. But it will cost us billions - money I'd rather see go on education, hospitals, infrastructure and so on, things that will benefit everybody. There is a social cost either way, and I'd rather the people who were caught out paid the price, not those that weren't. What message are we sending otherwise? Take any risk you like, and if it goes wrong - no problem, we'll tax other people and cut services to dig you out.Let the people who have a short and limited time on this planet get on with their lives and have a chance at happiness.0 -

Monty Burnz wrote: »Take any risk you like, and if it goes wrong - no problem, we'll tax other people and cut services to dig you out.

This is the hard problem, someone could afford ( objectively) to live in Tallaght and they managed to get a ridiculous mortgage for Terenure that they can no longer pay.

The solution involves moving them to where they can/could afford to live and perhaps writing off part of the debt if they agree to that solution.

It does not involve them getting a massive writeoff to stay in Terenure. Sorry. They took a risk and it backfired.

Nobody owns a home until it is paid off, there are cases where someone took no real risk , got to the end of a small mortgage and fell sick and into arrears. By all means be considerate there as it is a small amount of money and they cannot be housed elsewhere any cheaper.0 -

Monty Burnz wrote: »Unfortunately you don't seem to recognise that the cost of bailing out the foolish and the unfortunate will be borne by everybody - if it wasn't going to cost us billions, I'd be all for it. But it will cost us billions - money I'd rather see go on education, hospitals, infrastructure and so on, things that will benefit everybody. There is a social cost either way, and I'd rather the people who were caught out paid the price, not those that weren't. What message are we sending otherwise? Take any risk you like, and if it goes wrong - no problem, we'll tax other people and cut services to dig you out.

The private banking companies should be made to pay for this (and they should of done so from day 1 or been allowed to fail.)

I do not advocate that debts should be let off with at the flick of a switch but the debts we are laden with are in many cases overbearing and will never be paid off.

We have become enslaved to the banking system which we do not own in the slightest (they are still the powerful independant answer to no one entitys that they were pre crash.)

In relation to sending out a message of take any risk you could say the same about driving a car an then expecting health care if and when you crash it. Or smoking and expecting the same? I mean dont these people know and understand the risks before they did that? Dog eat dog. It's a cruel world.0 -

The private banking companies whose shareholders were totally wiped out? The ones now owned by the citizens of this country who pumped tens of billions into them? They will pay for the people who default, yes. It's the notion that they will also pay for people who want their debts written off and to keep the properties they borrowed for that I find offensive.The private banking companies should be made to pay for this (and they should of done so from day 1 or been allowed to fail.)

If they can't be paid, the debtor can go bankrupt. Simple.I do not advocate that debts should be let off with at the flick of a switch but the debts we are laden with are in many cases overbearing and will never be paid off.

The difference is that - with the exception of BOI - now they are working for us.We have become enslaved to the banking system which we do not own in the slightest (they are still the powerful independant answer to no one entitys that they were pre crash.)

People pay for car insurance and health insurance. When you smoke, most of the money you pay is tax. What you are proposing is a situation where people get insurance for their bad financial decisions without paying for it - rather everyone else has to pay for it. Why does this apply only to property? What about all the bank shareholders who lost their money? Why don't they get compensation under your philosophy? Many older people would have had all their savings in 'safe' bank shares to pay for their retirements - will you hand cash over to them too? If not, why not?In relation to sending out a message of take any risk you could say the same about driving a car an then expecting health care if and when you crash it. Or smoking and expecting the same? I mean dont these people know and understand the risks before they did that? Dog eat dog. It's a cruel world.0 -

Advertisement

-

As has been pointed out already, they already have. Or are you proposing that we go after anyone who ever owned shares in AIB and kick them out of their houses to sell them off to use the proceeds to keep delinquent mortgage borrowers in houses they haven't paid for.The private banking companies should be made to pay for this

You are misrepresenting the level of safety net involved here. If you crash your BMW the taxpayer will pay for your medical treatment through the HSE but will not pay for a new BMW for you. If you don't pay your mortgage and your house gets repossessed the tax payer will ensure that you are not left without a roof over your head, via the DSP, but will not give you a present of a new home in Foxrock.In relation to sending out a message of take any risk you could say the same about driving a car an then expecting health care if and when you crash it. Or smoking and expecting the same? I mean dont these people know and understand the risks before they did that? Dog eat dog. It's a cruel world.0 -

At no point have I advocated that the state or tax payer should bear the burden of these loans. In fact I was totally against the state bailing out a private profit making company through the banking guarantee scheme.

There are many different individual circumstances of people in different circumstances. For example: -

1/ people and families who are in ghost estates. never any hope of selling or moving or renting. Anyone who thinks they should shut up and pay for the rest of their lives in such awful conditions is just awful IMHO.

2/ Young couples and families who bought small just to get on the ladder and now are stuck in massive -ve equity with a growing family.

3/ people who stuck there knecks out too far because they literally believed that property was as easy as printing your own money.

and many others inbetween.

At least if we had a situation where people could in certain circumstances hand back the keys then they would have a chance of making a +ve difference to the economy and society.

I dont believe for a second that everyone would just up and try to do that as people homes mean more to them than just a place to stay.

Let the banks, many of whom have been in existence before I was I born and will be long after I die take this property and take a long term view as to recovering their 2 cents from it.

Let the people who have a short and limited time on this planet get on with their lives and have a chance at happiness.

Firstly, you're not connecting the dots here. The Irish taxpayer owns the banks. So every penny that is diverted to bailout a reckless borrower is a penny taken from funds to build roads, hospitals and schools.

Secondly, the people you are describing in your analogies are basically people like yourself. Because you screwed up and made bad choices in life, you now have an entitlement that someone else to has to pay for it. At the end of the day, you signed the contract and you need to behave like a mature adult and man to your personal responsibilities. I made poor choices myself in life, and have suffered far worse than anything the average person living in a ghost estate in negative equity has ever had to deal with. Yet I am not asking other people to give me a dig out.

Thirdly, if someone in negative equity hands back the keys of their house, the banks are *never* going to recover the money because house prices are not going to return to Celtic Tiger era levels. Anyone who believes that has learned nothing from what has happened during the last 5 years.0 -

Look like trouble for UK with their bank going to be downgraded tonight.

There will be lots of people with mortgages will be affected by this also.

http://news.sky.com/home/business/article/16250899

http://www.bbc.co.uk/news/business-18502003

http://www.bbc.co.uk/news/uk-politics-18535642

http://www.bbc.co.uk/news/world-europe-jersey-18517630

0 -

Monty Burnz wrote: »Unfortunately you don't seem to recognise that the cost of bailing out the foolish and the unfortunate will be borne by everybody - if it wasn't going to cost us billions, I'd be all for it. But it will cost us billions - money I'd rather see go on education, hospitals, infrastructure and so on, things that will benefit everybody. There is a social cost either way, and I'd rather the people who were caught out paid the price, not those that weren't. What message are we sending otherwise? Take any risk you like, and if it goes wrong - no problem, we'll tax other people and cut services to dig you out.

Monty i guess you dont own your own home ( not that makes me better than you ) But i find your words derogatory.

Can you answer me how people who did buy ( and cost the same as renting ) were foolish. Yes i agree a lot took the piss take

and went overboard but not everyone did. Most people brought a HOME for their CHILDREN to grow up in a stable enviroment. And also because we saw everything getting out of reach so jumped onboard while we could.

Now lets move on a few years and we have USC on every wage ( -€400 me and missues monthly ) and maybe wage cuts ( €10k ) and household tax / water charges / petrol hikes / doctors and dentists / or private health care ( lol ) ( just suffer the pain lads ) / TSB ( gouverment owned ) hiking their interest rate well above the norm and you might just get where we are coming from ( maybe €300 more than other banks a month ).

Now i have no kids and i have no idea how people are surviving who do have kids.

I guess in your world we kick every none payer ( paying but not the full amount, just what they can afford )out and leave empty decaying propertys and get the social to look after them ( costs you ). While all along you are paying USC to pay the bond holders who will never spend a cent in Ireland.

Are you on this plant or simpsons planet ?

and monty you are bailing out the foolish and unfourtanate faceless bankers but wont help your fellow country man ?

And the Banks DID cost you billions......0 -

Why, do you find yourself in the former category?Monty i guess you dont own your own home ( not that makes me better than you ) But i find your words derogatory.

So you got caught up in the frenzy of the bubble? And how is that everyone else's problem?Can you answer me how people who did buy ( and cost the same as renting ) were foolish. Yes i agree a lot took the piss take

and went overboard but not everyone did. Most people brought a HOME for their CHILDREN to grow up in a stable enviroment. And also because we saw everything getting out of reach so jumped onboard while we could. You made a very bad financial move. That's the price of freedom. If your property had doubled in value, would you have been happy if you were forced to hand the extra value over to someone who had not bought? Genuine question - please answer it.

Right...so? Did you assume nothing would ever go wrong when you took out your mortgage, allowing no margin of safety? If you did allow a margin, what happened to it?Now lets move on a few years and we have USC on every wage ( -€400 me and missues monthly ) and maybe wage cuts ( €10k ) and household tax / water charges / petrol hikes / doctors and dentists / or private health care ( lol ) ( just suffer the pain lads ) / TSB ( gouverment owned ) hiking their interest rate well above the norm and you might just get where we are coming from ( maybe €300 more than other banks a month ).

Costs me either way, doesn't it? It costs me to subsidise people who aren't repaying their debts too. And why would the property be 'empty and decaying'? Do you think nobody would want to buy it when the deadbeat borrower is out of it?Now i have no kids and i have no idea how people are surviving who do have kids.

I guess in your world we kick every none payer ( paying but not the full amount, just what they can afford )out and leave empty decaying propertys and get the social to look after them ( costs you ). While all along you are paying USC to pay the bond holders who will never spend a cent in Ireland.

You clearly have no idea what you are talking about. The bank owners have been totally wiped out. The taxpayer owns the rubble of the banks (bar most of BOI), and every loss inflicted on the Irish banks comes out of the pocket of the Irish taxpayer. The taxpayer is already subsidising non-payers with mortgage interest relief plus the 1 year moratorium on repossession, as well as massive forbearance. 15% or so of all mortgages are in arrears - but there are only about 200 repossessions per YEAR where the 'owner' hasn't abandoned the property.Are you on this plant or simpsons planet ?

and monty you are bailing out the foolish and unfourtanate faceless bankers but wont help your fellow country man ?

And the Banks DID cost you billions.....

I for one am sick of freeloaders at every level of our society.0 -

MysticalRain wrote: »Firstly, you're not connecting the dots here. The Irish taxpayer owns the banks. So every penny that is diverted to bailout a reckless borrower is a penny taken from funds to build roads, hospitals and schools.

Secondly, the people you are describing in your analogies are basically people like yourself. Because you screwed up and made bad choices in life, you now have an entitlement that someone else to has to pay for it. At the end of the day, you signed the contract and you need to behave like a mature adult and man to your personal responsibilities. I made poor choices myself in life, and have suffered far worse than anything the average person living in a ghost estate in negative equity has ever had to deal with. Yet I am not asking other people to give me a dig out.

Thirdly, if someone in negative equity hands back the keys of their house, the banks are *never* going to recover the money because house prices are not going to return to Celtic Tiger era levels. Anyone who believes that has learned nothing from what has happened during the last 5 years.

Thirdly, if someone in negative equity hands back the keys of their house, the banks are *never* going to recover the money because house prices are not going to return to Celtic Tiger era levels. Anyone who believes that has learned nothing from what has happened during the last 5 years.

I love the idea that people have that we own the banks. Maybe the rhetoric that has been spun by the political system wouuld have you believe that but they cannot even adjust senior salaries (nor or they even eager to ask) in fact aside from the cash input the banks as they have always been are essentially free agents to do as they please.

And to think that the banks wont ever make money is a bit like saying the casino 'house' will lose. I'm sorry but your naivity of the banking system is just so complete if you think that they will ever lose or fail to make a profit. Banks can make money by charging interest (money which doesn't even exist in the monetary system) so by default they will always be profit making machines at absolute top level of the money creation and making machine.0 -

What's good for the banks is good for us at this stage. When they ultimately return to profit (which could be 20 years away) we'll see some of our money back.I love the idea that people have that we own the banks. Maybe the rhetoric that has been spun by the political system wouuld have you believe that but they cannot even adjust senior salaries (nor or they even eager to ask) in fact aside from the cash input the banks as they have always been are essentially free agents to do as they please.

I'm sorry, but this just shows you haven't a clue about how banks work. You must have missed Anglo going bust and the other banks surviving only due to massive capital injections (and probably requiring more taxpayers' money yet). How does this tally with your very, very silly claim that they will 'never lose'?And to think that the banks wont ever make money is a bit like saying the casino 'house' will lose. I'm sorry but your naivity of the banking system is just so complete if you think that they will ever lose or fail to make a profit. Banks can make money by charging interest (money which doesn't even exist in the monetary system) so by default they will always be profit making machines at absolute top level of the money creation and making machine.0 -

Monty Burnz wrote: »Why, do you find yourself in the former category?

So you got caught up in the frenzy of the bubble? And how is that everyone else's problem? You made a very bad financial move. That's the price of freedom. If your property had doubled in value, would you have been happy if you were forced to hand the extra value over to someone who had not bought? Genuine question - please answer it.

Right...so? Did you assume nothing would ever go wrong when you took out your mortgage, allowing no margin of safety? If you did allow a margin, what happened to it?

Costs me either way, doesn't it? It costs me to subsidise people who aren't repaying their debts too. And why would the property be 'empty and decaying'? Do you think nobody would want to buy it when the deadbeat borrower is out of it?

You clearly have no idea what you are talking about. The bank owners have been totally wiped out. The taxpayer owns the rubble of the banks (bar most of BOI), and every loss inflicted on the Irish banks comes out of the pocket of the Irish taxpayer. The taxpayer is already subsidising non-payers with mortgage interest relief plus the 1 year moratorium on repossession, as well as massive forbearance. 15% or so of all mortgages are in arrears - but there are only about 200 repossessions per YEAR where the 'owner' hasn't abandoned the property.

I for one am sick of freeloaders at every level of our society.

2 words...Moral Hazard! Theres a feedback loop from a micro view point into a macro one in your thinking into why the Germans are so oppossed to eurobonds!0 -

Yeah, moral hazard. I'll tell you one thing - if people get away with freeloading it's going to deal a woeful blow to the whole fabric of our society as the people who did nothing wrong and made all the right decisions get screwed over in favour of the unlucky, the foolish and the greedy.2 words...Moral Hazard! Theres a feedback loop from a micro view point into a macro one in your thinking into why the Germans are so oppossed to eurobonds!0 -

I don't take at face value what the politicians tell me (if I did, I would no doubt own a house in negative equity now)I love the idea that people have that we own the banks. Maybe the rhetoric that has been spun by the political system wouuld have you believe that but they cannot even adjust senior salaries (nor or they even eager to ask) in fact aside from the cash input the banks as they have always been are essentially free agents to do as they please.

Regardless of whether bankers are giving the two fingers to the Irish taxpayer, the same taxpayer still funds them. The political classes in this country allow the bankers to get away with their high salaries because they too are in on the same scam.And to think that the banks wont ever make money is a bit like saying the casino 'house' will lose. I'm sorry but your naivity of the banking system is just so complete if you think that they will ever lose or fail to make a profit. Banks can make money by charging interest (money which doesn't even exist in the monetary system) so by default they will always be profit making machines at absolute top level of the money creation and making machine.

You still don't get it. The banks have already lost, and lost big time. Most of them would have gone bust already if the taxpayer hadn't poured billions into them. The only way a banks will ever recoup the losses from someone handing back the keys to their house is if house prices climb back to the levels they were at in 2007, and that just ain't going to happen. No amount of financial jiggery-pokery will change that.0 -

Advertisement

-

Monty Burnz wrote: »Unfortunately you don't seem to recognise that the cost of bailing out the foolish and the unfortunate will be borne by everybody - if it wasn't going to cost us billions, I'd be all for it. But it will cost us billions - money I'd rather see go on education, hospitals, infrastructure and so on, things that will benefit everybody. There is a social cost either way, and I'd rather the people who were caught out paid the price, not those that weren't. What message are we sending otherwise? Take any risk you like, and if it goes wrong - no problem, we'll tax other people and cut services to dig you out.

You have a point - I’m not in favour of blanket debt write-offs or those, who can afford to pay, being allowed to play a strategic non payment game hoping the tab will be picked up by “them” (i.e. the rest of us taxpayers). However, the mortgage arrears issue needs to be tackled purposefully and moved forward from the present uncertainty.

Some posters take a very rigid view of how to deal with the mortgage arrears issue and ridicule any approach other than foreclosure / repossession. They adopt a “green field” approach the problem, as if nothing is already happening and as if we have to start from scratch.

This is clearly not the case and, although progress may seem to be slow, quite a lot has already been happening, since publication of the Keane Report on mortgage arrears last September, for example:

• The Department of Finance Mortgage Arrears Report of January 2012, provides an update on the growth in mortgage arrears and on progress to date on driving / overseeing the implementation of the recommendations of the Keane Report: http://banking.finance.gov.ie/wp-content/uploads/Mortgage-Arrears-PDF.pdf

• Matthew Elderfield, speaking at a reception in Cork last October outlined the Central Bank’s strategy and concluded by saying:

“the mortgage arrears problem needs to be addressed on a case-by-case basis by lenders. This has been widely acknowledged, although perhaps not universally accepted”.

“this case by case approach will only work if the situation of unsustainable mortgages is addressed properly. As a result, the Boards of Directors and senior management of the lenders will be required by the Central Bank to formally reassess their approach to unsustainable mortgages”.

“the banks’ own actions need to take care not to exacerbate the arrears problem”.

“the banks need to have the operational capacity – including structure, resourcing and senior sponsorship – to address the arrears problem effectively, implementing best practice, rigorously tackling all the dimensions of the problem and ensuring compliance with the Code.”

• The Irish Times of 17th March 2012 contains an update on the deadline by which banks have to categorise their mortgages and produce solutions or “products” for each category: http://www.irishtimes.com/newspaper/finance/2012/0317/1224313471825.html

• On 6th June 2012, the Minister for Finance responded to questions on engagement with the banks on negative equity and on personal insolvency legislation: http://debates.oireachtas.ie/dail/2012/06/06/00114.asp

• Irish Examiner of 9th June 2012 reports on “Significant policy and operational changes in how Irish banks deal with mortgages and other loan arrears are to come into force in the coming months”: http://www.irishexaminer.com/archives/2012/0609/business/lenders-draw-up-plans-to-deal-with-mortgage-arrears-196742.html0 -

MysticalRain wrote: »You still don't get it. The banks have already lost, and lost big time. Most of them would have gone bust already if the taxpayer hadn't poured billions into them. The only way a banks will ever recoup the losses from someone handing back the keys to their house is if house prices climb back to the levels they were at in 2007, and that just ain't going to happen. No amount of financial jiggery-pokery will change that.

Interestingly I would take the opposite view! A great many banks (not all) over gambled. There are 'tiers' of banks from international, to national to local each with a variety of lending and money making options. The high level tier banks can create money and lend to governments for example. (these banks will almost inevitable never go bust because the money making mechanism must be protected. The lending of this money to govs and other banks is what people mistakingly call "growth", but infact its just debt being created.)

Anyway, by allowing our banks to become so big and so intertwined in every facet of our economy to the point where the government needed to step in and write a blank cheque for fear of total country meltdown IMHO means that we failed just as much as some banks did. One or 2 banks in particular were very bad.

In the casino analogy you could say that few blackjack tables were cleaned out but on the whole the 'house', or the banking system as a whole remains very much intact.

What we are seeing now is people wishing for currency devaulations to kick start their economies. This is typically good news for other banks around the world and countries that can exploit a now weakened economy by pillaging natural resources, services and goods for a fraction of the monetrary value they were once worth.

Anyway, that been said for anyone who really understands the absolute horror at how a fractionalised banking system works (the feds banking guide is a real eye opener on this and recommended reading) they would know that the money creation curve is pretty much about peaked out and the multi trillion commodities bubble that is currently circling the drain cannot be stopped.

In that regard it will be interesting to see how the real top world bankers play out their little monetary game on the people around the world.0 -

We don't even have "top bankers" Lantus but Lenihan wrote our lot a bigger cheque than any other state did.0

-

Why taxpayers must pay for reckless savers who was gambling by keeping their money in deregulated banks?MysticalRain wrote: »Firstly, you're not connecting the dots here. The Irish taxpayer owns the banks. So every penny that is diverted to bailout a reckless borrower is a penny taken from funds to build roads, hospitals and schools.

Why not to close insolvent banks like AIB and leave only one state owned bank?0 -

The banks were never 'deregulated'. I'm not sure why you think savers were 'reckless' unless they had savings that exceeded the deposit guarantee - and even then, where would you suggest they should keep these savings? Under the mattress?Count Dooku wrote: »Why taxpayers must pay for reckless savers who was gambling by keeping their money in deregulated banks?

They should have been allowed go bust - but of course the government would still be on the hook for a lot (probably most) of savings due to the deposit guarantee. Of course the credit unions would also have been wiped out too.Count Dooku wrote: »Why not to close insolvent banks like AIB and leave only one state owned bank?

If you think we are seeing 'austerity' and 'pain' now, you can imagine how things would have been when the ATMs stopped working and the shops ran out of food. Even present-day Greece would look pretty cushy by comparison.

(of course, after a year or two, I think our recovery would have been a lot faster - but plenty of people would be dead)0 -

Ulsterbank, rabobankMonty Burnz wrote: »The banks were never 'deregulated'. I'm not sure why you think savers were 'reckless' unless they had savings that exceeded the deposit guarantee - and even then, where would you suggest they should keep these savings? Under the mattress?

Do you mean that media are hiding truth about thousands of dead in Iceland?Monty Burnz wrote: »They should have been allowed go bust - but of course the government would still be on the hook for a lot (probably most) of savings due to the deposit guarantee. Of course the credit unions would also have been wiped out too.

If you think we are seeing 'austerity' and 'pain' now, you can imagine how things would have been when the ATMs stopped working and the shops ran out of food. Even present-day Greece would look pretty cushy by comparison.

(of course, after a year or two, I think our recovery would have been a lot faster - but plenty of people would be dead)0 -

What about them? You understand that Ulsterbank's parent company had to be bailed out just like the Irish banks?Count Dooku wrote: »Ulsterbank, rabobank

Ireland is not Iceland, in spite of what ULA propaganda would have you believe. They never nationalised their bank debt, they have their own currency, they had to introduce currency controls (which would be illegal here), they've had massive inflation (up to 16% in 2009) and their standard of living has dropped substantially.Count Dooku wrote: »Do you mean that media are hiding truth about thousands of dead in Iceland?

Pretending that Iceland has somehow gotten away with their crash and everything is suddenly fine there is just completely dishonest.Iceland’s crisis-management policies are creating the island’s next property bubble less than four years after its banking meltdown threw the economy into its worst recession.

Prices for new homes touched a record last quarter, having surged 40.1 percent since the final three months of 2010, according to estimates by the National Registry of Iceland in Reykjavik. Average house prices have risen 11.3 percent since the market bottomed at the end of 2009, according to central bank data at the end of the first quarter.

Currency controls imposed in 2008 and designed to protect the island of 320,000 from a mass capital exodus are now channeling funds into a market that is showing symptoms of overheating and driving home-loan debt higher. Close to $8 billion in kronur are held by offshore investors unable to get their money out of the country, according to Arion Bank hf economist Thorbjorn Sveinsson. As the government signals restrictions will remain until at least 2015, funds are flowing into one of the few longer-term investment options: real estate.

“If the development continues without interference, this will lead to a property bubble within the next two years,” Asgeir Jonsson, an economist at Reykjavik-based asset manager Gamma, said in an interview. “There’s a greater risk of an asset bubble being created in an economy that is closed off behind capital controls.”

Iceland is still a mess - it's just a different flavour of mess.0 -

British taxpayers will have to pay itMonty Burnz wrote: »What about them? You understand that Ulsterbank's parent company had to be bailed out just like the Irish banks?

I don't see standards of living improving hereMonty Burnz wrote: »Ireland is not Iceland, in spite of what ULA propaganda would have you believe. They never nationalised their bank debt, they have their own currency, they had to introduce currency controls (which would be illegal here), they've had massive inflation (up to 16% in 2009) and their standard of living has dropped substantially.

Pretending that Iceland has somehow gotten away with their crash and everything is suddenly fine there is just completely dishonest.

Iceland is still a mess - it's just a different flavour of mess.

Difference that Iceland will exit recession much earlier than Ireland, while Ireland will have to pay for idea to preserve banks at any costs for at least two decades

Iceland on growth path, but hard road ahead - ReutersIn August, Iceland exited its $2.1 billion (1.3 billion pound) International Monetary Fund bailout programme and the economy grew 2.5 percent in the first half of the year. That is slow compared to before the crisis, when the economy regularly rose 5 percent a year.

But Greece is likely to contract by more than five percent this year and won't grow until 2013 at the earliest.

Iceland expects a balanced budget in 2014 and returned to the international capital markets in March.

Once poster child of crisis, Iceland recovers - ReutersIceland's GDP growth estimated at some 2.6 percent this year will outshine even powerhouses like Sweden.

"These are among the highest numbers in Europe," said Finance Minister Steingrimur Sigfusson. "Sometimes it is easier to turn a small boat around than a big ship."

Currency depreciation though is only part of the picture.

Capital controls, progressive taxes and a careful phasing-in of austerity measures were also key to getting the country back on track, bringing a more than 10 percent fiscal deficit back to a near balance.

Iceland also did what other parts of Europe haven't dared to do - let its banks go under. It took some of the cost itself but forced foreign creditors to take the biggest hit.0 -

What does this have to do with your point regarding 'irresponsible savers'?Count Dooku wrote: »British taxpayers will have to pay it

A few points - we are not Iceland, and we never were. The options they had were not available to us as I have already said. They are still in a big, big mess. And I've already said that the banks should have been allowed fail.Count Dooku wrote: »I don't see standards of living improving here

Difference that Iceland will exit recession much earlier than Ireland, while Ireland will have to pay for idea to preserve banks at any costs for at least two decades

So I'm not sure what point you are making.0 -

Advertisement

-

I think people are mistaking what actually happened in Iceland.

It wasn't a case of them deciding not to put a penny into the banks and letting them go. In terms of GDP, since 2008 they are second only to Ireland in terms of the amount of money they pumped into the banks. They did absolutely everything they could to keep them afloat and only let them go bust when they had no other choice. They wouldn't have been able to socialise the bank debt as it was completely unsustainable and would have lead to a sovereign default pretty quickly.

The only reason Ireland managed to get away with socialising it and not defaulting was because we are backed up by the EU/Eurozone.

Naturally, actually socialising the debt was a huge mistake by Ireland. This doesn't mean however that we should just go ahead and make another mistake by socialising the losses of mortgage holders too, which given the Irish people now effectively own the banks is what people are suggesting.0 -

Naturally, actually socialising the debt was a huge mistake by Ireland. This doesn't mean however that we should just go ahead and make another mistake by socialising the losses of mortgage holders too, which given the Irish people now effectively own the banks is what people are suggesting.

We own the massive debt but we dont have any actual ownership on the banks in terms of control. Even the government can only try to 'persuade' banks to change variable rates. They dont have any real control.0 -

I think you need to make a distinction between the banks saying 'fuсk you, I won't do what you tell me' and the banks explaining to the government that reducing variable rates by X will have a negative effect of Y million per month on the their cash flows, a difference that will need to be funded by the state.We own the massive debt but we dont have any actual ownership on the banks in terms of control. Even the government can only try to 'persuade' banks to change variable rates. They dont have any real control.0 -

Yes, exactly. The main problem is that the state can't be sure when the bank management are blowing smoke up their arses.Unrealistic wrote: »I think you need to make a distinction between the banks saying 'fuсk you, I won't do what you tell me' and the banks explaining to the government that reducing variable rates by X will have a negative effect of Y million per month on the their cash flows, a difference that will need to be funded by the state.0 -

Naturally, actually socialising the debt was a huge mistake by Ireland. This doesn't mean however that we should just go ahead and make another mistake by socialising the losses of mortgage holders too, which given the Irish people now effectively own the banks is what people are suggesting.

There are strong views on both sides of the mortgage arrears debate and for good reason – socialising any more debt will not be welcomed by taxpayers, who have been prudent in their financial affairs.

But, however strongly people may feel about how it should be handled, the reality is that Government and the state’s independent Central Bank have been implementing policies aimed at helping those in arrears to resolve their own debt problems. It remains to be seen just how successful this approach will be and how much more it will cost the taxpayer.

On 25 May 2012, the Central Bank published its report on Residential Mortgage Arrears and Repossessions Statistics: Q1 2012 (http://www.centralbank.ie/press-area/press-releases/Pages/ResidentialMortgageArrearsandRepossessionsStatisticsQ12012.aspx).

This report covers statistics on arrears, restructuring arrangements and legal proceedings / repossessions. It also provides a link to the guide to completing the Standard Financial Statement (‘SFS’), used by lenders when assessing whether or not to offer alternative repayment arrangement and what type of arrangement is appropriate (under the Mortgage Arrears Resolution Process, ‘MARP’).

Honesty and good faith are cornerstones of the process. For example, the guide states that:

“it is important that you include all your basic living expenses in the SFS. You should fill out the form honestly and provide any documentation your lender asks for. If you do not, you can be classified as not co-operating with your lender and the 12 month waiting period (moratorium) for beginning legal action for repossession of your property will no longer apply to you”.

I’m tempted to be cynical about the honesty of the process and, certainly, it carries risks of abuse and corruption (as mentioned by other posters). But burdening people for life with unsustainable debt is no panacea either, as people can go to the UK to avail of bankruptcy laws that are much more benign than ours, resulting in even more cost to the taxpayer.

What other realistic options are there?0 -

Central Bank figures 'overstating' number in mortgage crisis

OFFICIAL figures on the "mortgage crisis" overstate the number of households in real trouble – and lack key insights into how deep the problem really is.

An investigation by the Irish Independent has revealed the Central Bank's figures include several types of borrowers who are no longer in trouble.

A large number of senior bankers right across the industry who spoke to the Irish Independent now insist the situation is improving.

http://www.independent.ie/national-news/central-bank-figures-overstating-number-in-mortgage-crisis-3147111.html

I see institutions like the central bank as part of the problem, not the solution.0 -

Advertisement

-

This particular topic has been debated at this stage for a number of years, yet it remains in political limbo largely because either introducing it or ruling it out definitively will result in a loss of votes, one way or another, for the government that does so. So, I wouldn't hold my breath that it will be tackled anytime soon.

Problem is, that as long as it does remain an undefined possibility, you're going to see people holding out for it, and naturally, this is not going to help us as a society.

The uncertainty surrounding this is now probably doing more harm than the consequences of actually choosing to do so or not as many of those holding out would either not qualify or simply not like the conditions of any such scheme, if we introduced one (some are hoping for a no-strings attached model and would balk at the thought of giving up equity for forgiveness), and would be forced to actually begin repaying their mortgages, given they can no longer hold out for a future white knight.0 -

MysticalRain wrote: »Central Bank figures 'overstating' number in mortgage crisis

OFFICIAL figures on the "mortgage crisis" overstate the number of households in real trouble – and lack key insights into how deep the problem really is.

An investigation by the Irish Independent has revealed the Central Bank's figures include several types of borrowers who are no longer in trouble.

A large number of senior bankers right across the industry who spoke to the Irish Independent now insist the situation is improving.

http://www.independent.ie/national-news/central-bank-figures-overstating-number-in-mortgage-crisis-3147111.html

I see institutions like the central bank as part of the problem, not the solution.

Interesting to see that a large number of senior bankers have been saying to the Irish Independent that the level of reporting by Central Bank is not deep enough. I take it this means they want even more stringent regulatory reporting requirements placed on their industry.

They also protest that the real figures are better than those published (even though, I'm quite sure they were well consulted by Central Bank people about the existing reporting requirements).

I see these “howls of protest” from bankers as good sign that the Central Bank is, indeed, on the right track. I trust they will stick to their task and maybe get the bankers to deliver on their desired higher standard of reporting as well.

What a change from their pre-bailout position of wanting only “lite regulation” – they now can’t get enough of it – are we witnessing an historic “St. Paul on the road to Damascus moment” from bankers?

I agree with The Corinthian’s point about the uncertainty being caused by delay in implementing the new Personal Insolvency legislation – the quicker the better the bill is published as the next step in resolving this issue.

In this regard, Alan Shatter, Minister for Justice, Equality & Defence, is reported in the Irish Times of 18th June as saying that the Personal Insolvency Bill (200 pages at the moment) will be published by the end of the month: http://www.irishtimes.com/newspaper/breaking/2012/0618/breaking51.html.0 -

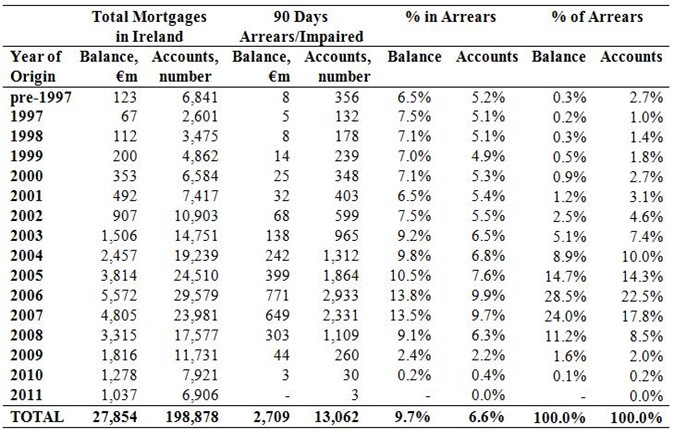

There is a big 'hidden' problem, this comes with 2 distinct strands. There are some €180bn+ of Mortgages in Ireland.

Half are not our problem. They are either held by non covered institutions, BOSI/UB/IIB/FA/NIB would be the bigger ones. Or else they are seuritised and held by a Debt Vehicle.

Half are our problem as they are on the books of the covered institiutions AIB/BOI/INBS/EBS

The data on this mess is variable in itself. Here is a pretty fair comment on it.

http://www.centralbank.ie/stability/Documents/Mortgage%20Conference/Session%201/Paper%201/Paper.pdfThis sample represents a substantial portion of the country’s total outstanding residential loans,

indeed Central Bank of Ireland (2011b) shows that at the end of December 2010 786,164 mortgage

loans remained outstanding in Ireland, these were worth approximately €117 billion. It must be

noted that this CBI figure does not include BTL loans. For comparison, the loan-level figures, net

of the BTL market segment, constitute 521,000 loans valued at €68 billion, i.e. approximately 60

per cent of the national figure at the end of 2010. Further, although the four FMP institutions

comprise a large proportion of the overall mortgage market in Ireland it is not expected that the

data examined here are necessarily representative of the non-FMP institutions.

So the arrears data we get is not fully representative of the entire market and indications are that the non reported sections are less managed and with worse arrears that the more managed and widely reported sections.

The single most stressed 'group' are the BTL Mortgagees whose interest only period has expired and who are expected to repay...and cannot. Then there is cross comtamination to primary residences from that...eg 74k loans are secured on 63k properties eg Topup Loans used to but in Bulgaria and the like.The data contains approximately 74,000 loans in arrears at the end of 2010, associated with

63,000 properties. Of these, 24,011 properties have at least three months worth of repayments

outstanding on their mortgages. Unsurprisingly, the largest cohorts of borrower types (FTB- and

Mover-P&I borrowers) account for the majority of the 90DPD arrears balance (58 per cent), they are

in general better performing, with less than five per cent of their mortgaged properties in 90DPD,

than the groups which make up a smaller section of the mortgage book and whose repayments

are on an interest only basis. For example, BTL-IO borrowers have the highest arrears balance per

property (€2,100) of all borrower groups, this is of particular concern as these borrowers are the third

largest borrower group in the data, accounting for 12 per cent of all outstanding balances.

The cross contamination effect means that someone not in trouble on their main loan could be in trouble because they bought in Bulgaria....so what are we supposed to 'bail out' here???

Frankly I see writedowns being suitable for those with no further loans who got into trouble through unemployment or illness or both. The rest will have to go into administration or bankruptcy and that is that.

Bank of Ireland manages its mortgage book pretty well and therefore only has around half the arrears that eg BOSI has. Even in the more highly stressed cohorts (2006 Buyers) its arrears are below the market.

However if we look at their pre 1997 mortgages in arrears, 7000 of them for a gross value of €123m we see the average outstanding balance is €17.5k so chucking them out will cost the taxpayer more than a writedown might......and although we could probably sell the house and pay off the entire mortgage we will probably find them on the local housing list. We should look at something like a lien or registered interest in those cases like the Nursing Home clawback scheme. 0

0 -

MysticalRain wrote: »Central Bank figures 'overstating' number in mortgage crisis

OFFICIAL figures on the "mortgage crisis" overstate the number of households in real trouble – and lack key insights into how deep the problem really is.

An investigation by the Irish Independent has revealed the Central Bank's figures include several types of borrowers who are no longer in trouble.

A large number of senior bankers right across the industry who spoke to the Irish Independent now insist the situation is improving.

http://www.independent.ie/national-news/central-bank-figures-overstating-number-in-mortgage-crisis-3147111.html

I see institutions like the central bank as part of the problem, not the solution.

An investigation by the Irish Independant eh? The same Irish Independant that has Brendan "Green Jersey" Keenan as Economics editor? The man who loudly told Morgan Kelly on live TV that "We know what the Irish banks bad loans are. They're going to be about 1% of their loanbook"

But that apart, lets see what the Irish Independants fearless investigation has turned up:

"A large number of senior bankers right across the industry who spoke to the Irish Independent now insist the situation is improving."

Oh right - the Irish Independant asked some bankers if they were in trouble. The bankers said everythings fine. Irish Independants fearless reporters strike again.

Jaysus.0 -

Oh right - the Irish Independant asked some bankers if they were in trouble. The bankers said everythings fine. Irish Independants fearless reporters strike again.

Jaysus.

Substitute the Irish Cental Bank for the Indo and we get the lead up to the banking crisis.

Jaysus, in a Vincent Browne tone!")

Mad Men's Don Draper : What you call love was invented by guys like me, to sell nylons.

0 -

Advertisement

-

Substitute the Irish Cental Bank for the Indo and we get the lead up to the banking crisis.

Jaysus, in a Vincent Browne tone!

Very amusing analogy but I’m not sure it’s very helpful in informing people’s understanding about current handling of the mortgage arrears issue.

However about the management of the Indo, I’d agree that the bank regulatory function in Ireland between 2003 and 2010 proved a disaster. In this regard, I wouldn’t fault the view expressed by UK MP, Nigel Farage, to the effect that “the banking collapse was caused, more than anything, by bad government policy and the total failure of bad regulation.”

Most of us didn’t know it at the time (or more suspected it but didn’t want to know), but between 2003 & 2010, the Financial Regulator and Government effectively slept on the job. Meanwhile, we had a spending splurge and property bubble, on borrowed cheap money. Not surprisingly, we are all a bit miffed now that the final bill has come in, while those that drove the collapse “walked” with truckloads of compensation for early retirement.

In Ireland (along with most other Eurozone states, except, perhaps, Germany) we voted for the politicians who promised to give us the most goodies, without worrying us about how these goodies would have to be paid for. We now know what we should have known all along and unfortunately, it has left us with a sizable number of people who can’t or won’t make their mortgage repayments.

We are now in a space where we have to get our financial affairs in order, face up to and deal with the problem.

I’m as pissed off as anyone else about how we got here. I’m also just as sceptical about the political will to see through the cure being overseen by the Central Bank.

But what’s the alternative? A re-vamped Financial Regulatory regime has been put in place and new people appointed to see it through. I too am tempted to resort to cynicism, but at this stage, I’m willing to give the new people a chance.0 -

Definitely the wont pay need to be identified and brought to rights, it would be hard going to identify these genuinely.

After that it needs to be looked at to see if te banks behaved appropriately. There are many many instances where the bank screwed round the numbers to give out mortgages where they shouldn't have. I wouldn't agree with evictions in these cases and a system of right downs would be appropriate rather than it just happen at the banks discression. Like it or not the state have responsibility as there was effectively no regulation or control of banking.

In the remainder of cases we definitely need a system in place where swift solutions are out in place. I'm not adverse to solutions that see families stay in the houses and the banks/state/nama retain part ownership.

Are you suggesting that the banks forced these people to take out morgages they couldnt afford? Who put a gun to the heads of these people?

If a person borrowed money, they should repay it. Maybe not possible to do it in the time frame initally agreed, but that can be re negotiated. In other parts of the world, 50, 60 even 100 year morgages are not un common.

Personally, I'm paying my morgage; it isnt as affordable as I thought it would be when we started out (ie before sprog no.2 arrived, and then other half let go), but we are managing. I DO NOT want to pay for sombody else who took out a loan they now find difficulty in re paying, but who cant be arsed trying to find a workable solution0 -

Are you suggesting that the banks forced these people to take out morgages they couldnt afford? Who put a gun to the heads of these people?

If a person borrowed money, they should repay it. Maybe not possible to do it in the time frame initally agreed, but that can be re negotiated. In other parts of the world, 50, 60 even 100 year morgages are not un common.

Personally, I'm paying my morgage; it isnt as affordable as I thought it would be when we started out (ie before sprog no.2 arrived, and then other half let go), but we are managing. I DO NOT want to pay for sombody else who took out a loan they now find difficulty in re paying, but who cant be arsed trying to find a workable solution

You're quite right that people should repay their borrowings. As regards renegotiation of terms, options for banks to work on have been set out in the Keane report on Mortgage Arrears and, AFAIK, Central Bank has been urging banks to develop renegotiated solutions along the lines suggested (and to develop and resource other workable solutions themselves).

The key points are that there is no blanket debt forgiveness solution and each situation has to be dealt with on a case by case basis.

Issues in this regard are covered to some extent in earlier posts and, if you care to read it, in the Keane Report available from the Department of Finance website.

For those whose financial circumstances are impossible to handle within the above mentioned solutions, there is the Personal Insolvency Bill, due for publication tomorrow. But at 200 pages, this will take a bit of time to read and digest.0 -

The long awaited Personal Insolvency Bill was published today. Progress at last – it’s early days and reaction from opposition parties will be interesting.

According to Department of Justice and Equality site today, Minister Shatter “stated that "the Bill provides concrete options for those genuinely unable to discharge their financial obligations as opposed to those who can but won’t do so." Moreover, he noted that if creditors fail to constructively engage in the DSA or PIA process or if agreement does not prove possible, the option of initiating an application for a court adjudication of bankruptcy is available both to creditors and to an insolvent debtor.

Minister Shatter also reiterated that the Bill does not provide for the automatic writing-off of negative equity, where such may exist. Where a person is in a position to service their mortgage or other debt obligations, they must continue to do so. This Bill does not relieve solvent debtors of their responsibility to meet their contractual obligations”.

The site also provides details of the main provisions of the bill plus a link to the text of the bill.

(http://www.inis.gov.ie/en/JELR/Pages/PR12000198)

Much of the contents of the bill have already been in the public domain and it remains to be seen how long it will take before it is finally passed into law.0

Advertisement